Investing in Real Estate – A Guide to Investment Strategies

LINKEDIN

LINKEDIN

FACEBOOK

FACEBOOK

TWITTER

TWITTER

EMAIL

EMAIL

9 mins

9 mins

Download

Download

Share

Share

By proceeding you confirm that you are a resident of Australia or New Zealand accessing this website from within Australia or New Zealand and you represent, warrant and agree that:

- you are not in the United States or a “U.S. person”, as defined in Regulation S under the U.S. Securities Act of 1933, as amended (“U.S. Person”), nor are you acting for the account or benefit of a U.S. Person;

- you will not make a copy of the documents on this website available to, or distribute a copy of such documents to, or for the account or benefit of, any U.S. Person or any person in any other place in which, or to any other person to whom, it would be unlawful to do so; and

- the state, territory or province and postcode provided by you below for your primary residence in Australia or New Zealand are true and accurate.

Unfortunately, legal restrictions prevent us from allowing you access to this website. If you have any questions, please contact us by e-mail by clicking on the link below.

Securitisation and the increased sophistication of the real estate industry has found new ways to repackage real estate assets to create a broader menu of investment strategies and opportunities. However, the risk/return attributes, not to mention the liquidity, of these investment opportunities can vary greatly.

This paper provides a brief overview of the different real estate investment strategies based on risk-return styles – core, value-added and opportunistic and the four quadrants of real estate investing – classifying real estate investments based on whether they are equity or debt and traded in the public (listed) or private markets.

1.0 RISK – RETURN STYLES

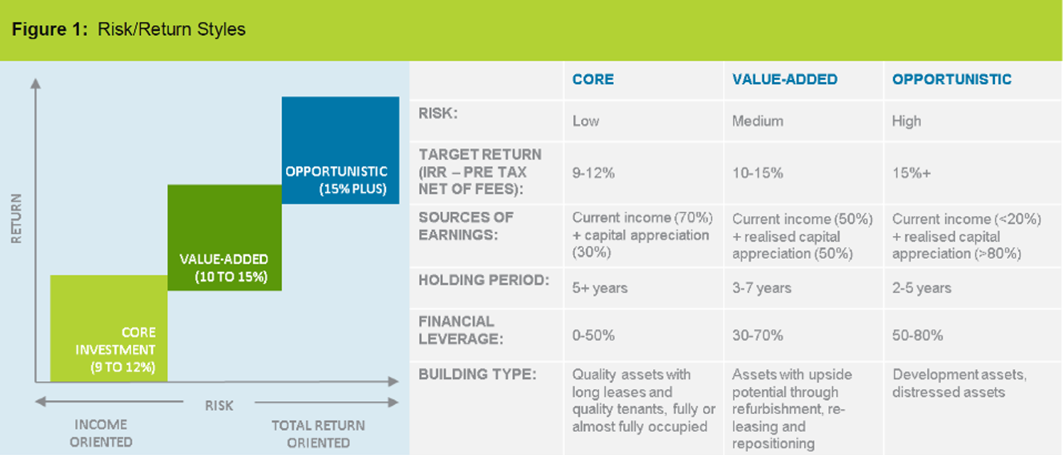

There are three key risk-return styles for real estate investing – core, value-added and opportunistic (Figure 1).

Core real estate investing is buying assets that are well located, leased to quality tenants and funded with modest levels of leverage. Such investments typically target 9%-12% p.a. total returns with the objective of providing investors with secure income plus modest capital appreciation. The income component typically represents a significant majority (circa 70%) of the expected total return. Examples of core investments include CBD office buildings, retail centres and industrial warehouses.

The ability to significantly enhance the value of core real estate is limited compared to value-added and opportunistic investment strategies. Core assets generally require little or no short-term capital expenditure other than normal repairs and maintenance.

However, core investing does not mean passive management of an asset.

Active management of core assets can add value through management initiatives such as managing lease profiles and reducing building operating costs.

Core real estate tends to be held for the long-term, typically 5 years or more. Leverage is generally below 50% - a core investor tends not to use high leverage to enhance investment returns.

In recent years real estate related social infrastructure such as child-care centres, medical centres and student accommodation have increasingly been considered as legitimate core investments. There are a number of listed and unlisted real estate funds focusing specifically on these sectors such as the Folkestone Education Trust and the Generation Healthcare REIT which are both listed on the ASX and the unlisted Australian Unity Healthcare Fund.

1.0 RISK – RETURN STYLES CONT’D

Value-added investing engages in active strategies to create value in the underlying real estate investments through refurbishment, re-development and/or leasing-up of vacant space. A value-added strategy typically targets

‘secondary’ assets which for various reasons have depressed levels of income or the value has deteriorated over time relative to the broader market. Through hands on ‘active management’ there is a focus on increasing an asset’s income and hence capital value. Value-added real estate investments will therefore appeal to investors seeking enhanced returns in exchange for higher levels of asset operating risk.

Value-added investments offer opportunities for a more balanced mix of income and capital growth than either a low risk core strategy or a higher risk opportunistic strategy. These investments target returns between 10%-15% p.a. and typically use modest to high levels of leverage of between 30% and 70%.

Value-added investments tend to have a hold period of between 3 and 7 years, although often the hold period is at the shorter end, as the successful execution of the strategy will often be dependent on picking the right time in the real estate cycle to exploit the value-added opportunity and maximise the investment return.

Opportunistic investing targets a range of higher risk strategies such as real estate development, highly leveraged financing or transactions involving

“turnaround” potential (often known as distressed investing), investments with complicated financial structures (including mezzanine debt) or emerging market investments.

The focus is on capital appreciation, with the returns typically back-ended and achieved through a sale or completion of a development; often with very little income along the way.

Such strategies usually use higher levels of leverage between 50% and 80% and typically target returns of 15% p.a. plus.

Opportunistic strategies require specialised investment and management expertise due to their complexity and to mitigate the higher risk that is associated with such strategies. Opportunistic investors tend to be sophisticated, well capitalised and have a higher risk appetite and are comfortable with higher levels of leverage than a core or value-added investor.

Opportunistic investing looks at relatively short-term hold periods – typically less than 5 years, and in many cases less than 3 years. The key is to expeditiously exit the investment as the investment strategy is executed and value maximised.

Value-added and opportunistic investing in most cases is not simply the use of high levels of leverage in real estate strategies. It is about careful analysis of the real estate cycle and market trends to take advantage of dislocations and mispricing in the market to produce superior investment returns.

2.0 FOUR QUADRANT INVESTING

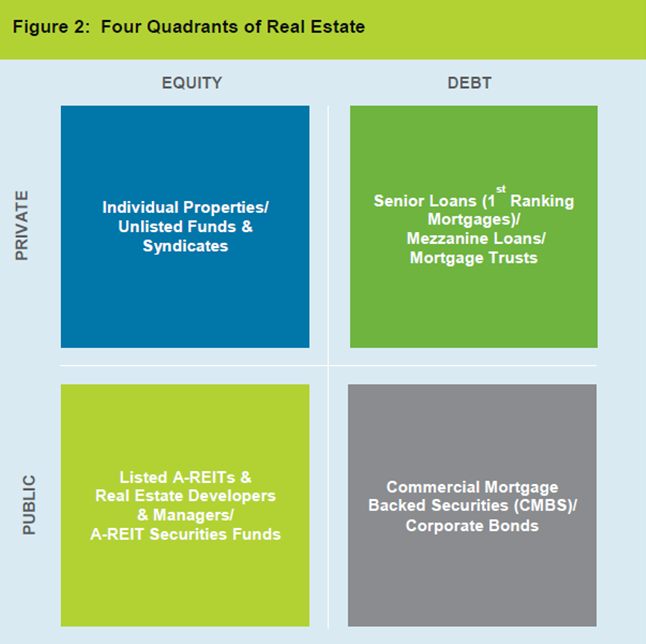

Four quadrant investing refers to the classification of real estate investing across all of the real estate related financial markets - public and private, debt and equity (Figure 2).

Private equity represents direct equity investments in individual buildings or unlisted funds/syndicates that own real estate assets. These investments are traded in the private market, and in between purchase and sale, the values of such investments are derived from valuations. As a result of being traded in the private market these real estate investments are relatively illiquid compared to the public market traded investments.

2.0 FOUR QUADRANT INVESTING CONT’D

The most common forms of private equity real estate investment in Australia, outside of directly owning a building, are unlisted real estate funds that hold a portfolio of assets or unlisted real estate syndicates which typically own one asset such as an office building or retail centre and have a fixed-term of between 5 and 7 years.

Public equity refers to investments in real estate investment trusts (A-REITs) or real estate companies whose securities or shares are traded on a stock exchange such as the ASX. The Australian A-REIT market is the most liquid and transparent of the four quadrant markets in Australia. According to the ASX, the A-REIT sector now comprises 50 A-REITs with a market capitalisation in excess of $97bn. There are another 29 real estate related securities that are classified by S&P/ASX as real estate managers and developers.

Private debt represents investments in direct real estate loans or in funds that hold mortgages on real estate (mortgage trusts). The loans maybe first mortgages (senior debt) or second ranking sub-ordinated loans such as mezzanine loans. When investing in real estate debt, the investor is essentially lending funds to an owner, purchaser or developer of real estate. Typically, the investor/lender will receive periodic interest payments from the borrower and a security charge against the property in the form of a mortgage. At the end of the mortgage term, the investor/lender will receive the balance of the mortgage principal. This type of real estate investing is similar to investing in bonds that are held to maturity.

Public debt represents real estate debt instruments such as commercial mortgage back securities (CMBS) which are traded in the public market or unsecured debt (corporate bonds) issued by A-REITs and real estate companies. Access to investing in the public real estate debt market in Australia is almost exclusively limited to institutional or ‘wholesale’ investors.

2.0 FOUR QUADRANT INVESTING CONT’D

The four-quadrant model of investing emphasises the links between real estate and the capital markets. The income from each of these investments relies on the performance of the underlying real estate despite the fact that the pricing, the risk and the liquidity will depend on which part of the spectrum (debt or equity) the investment occurs and whether it is traded in the public or private market.

3.0 CONCLUSION

Whilst the menu of real estate investment opportunities has increased, not all investment styles and strategies across the four quadrants are suitable for all investors.

The final decision will depend on their risk and return objectives and liquidity requirements.

Most investors in real estate will focus on core real estate strategies and will typically invest in the quadrant that best suits their liquidity requirements. If liquidity is an important factor, an investment in public equity such as A-REITs may be a more viable investment alternative than private real estate either directly or through an unlisted fund or syndicate.

Given the different markets and risk profiles, pricing anomalies in the short-term may occur across the three investment styles and four quadrants. A more sophisticated investor may take advantage of these pricing arbitrages and move across the three styles or allocate between the four quadrants according to where they expect to achieve the best relative risk-adjusted returns at different points in the real estate cycle.

Related News

Charter Hall acquires $445 million Sonic Healthcare life science facility on a 20-year triple-net sale and leaseback

Read more.tmb-news.jpg?Culture=en&sfvrsn=96db9902_1 "Office")

APPF Commercial and Charter Hall reach agreement on Sydney CBD assets

Read more

Charter Hall and WSI secure O’Brien as first anchor tenant at Western Sydney International Airport Business Precinct

Read moreTalk to us

Thanks for your interest in Charter Hall. Fill in your details below and we’ll get back to you as soon as possible.

I am interested in

Enquiry

*Indicates that this field is required.

All personal information submitted will be treated in accordance with our privacy policy.

By registering and/or submitting personal data to Charter Hall, you agree that, where it is permitted by law and in accordance with our Privacy Statement or where you have agreed to receive communications from us, Charter Hall may use this information to notify you of our products and services and seek your feedback on our products and services. Please note you can manually opt out of any communications.

-

© Charter Hall Group, 2026.

- Terms of Use

- Privacy Policy

- Complaints Guide