Early Learning Centres – An Attractive Real Estate Investment

LINKEDIN

LINKEDIN

FACEBOOK

FACEBOOK

TWITTER

TWITTER

EMAIL

EMAIL

7 mins

7 mins

Download

Download

Share

Share

By proceeding you confirm that you are a resident of Australia or New Zealand accessing this website from within Australia or New Zealand and you represent, warrant and agree that:

- you are not in the United States or a “U.S. person”, as defined in Regulation S under the U.S. Securities Act of 1933, as amended (“U.S. Person”), nor are you acting for the account or benefit of a U.S. Person;

- you will not make a copy of the documents on this website available to, or distribute a copy of such documents to, or for the account or benefit of, any U.S. Person or any person in any other place in which, or to any other person to whom, it would be unlawful to do so; and

- the state, territory or province and postcode provided by you below for your primary residence in Australia or New Zealand are true and accurate.

Unfortunately, legal restrictions prevent us from allowing you access to this website. If you have any questions, please contact us by e-mail by clicking on the link below.

Folkestone is the leading provider of early learning accommodation in Australia and New Zealand with 402 long day care centres – owned by the ASX listed Folkestone Education Trust (FET).

Folkestone has 27 operators currently operating its centres. Goodstart Early Learning, the not for profit operator formed by four Australian charitable groups in 2009 to take over most of the Australian centres previously run by ABC Learning Centres, operates more than 650 centres nationally, 240 of which are owned by FET.

Demand Drivers

Demographic and socio-economic changes continue to drive the demand for early learning accommodation.

Early learning is now seen as both a mechanism to support labour force participation (particularly driven by the increase in female participation in the workforce) and an important form of early learning and education.

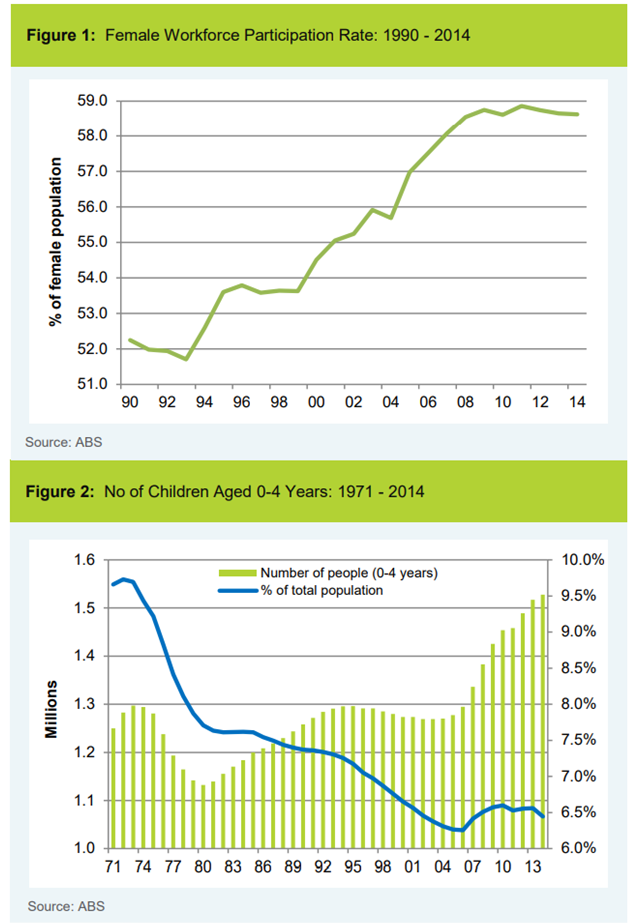

The number of females working has increased substantially since the 1970’s. The proportion of women working has increased from 43% in the late 70’s to just under 60% (Figure 1). The Grattan Institute has estimated that if six per cent more women entered the paid workforce, the size of the Australian economy would increase by about $25 billion per year.1

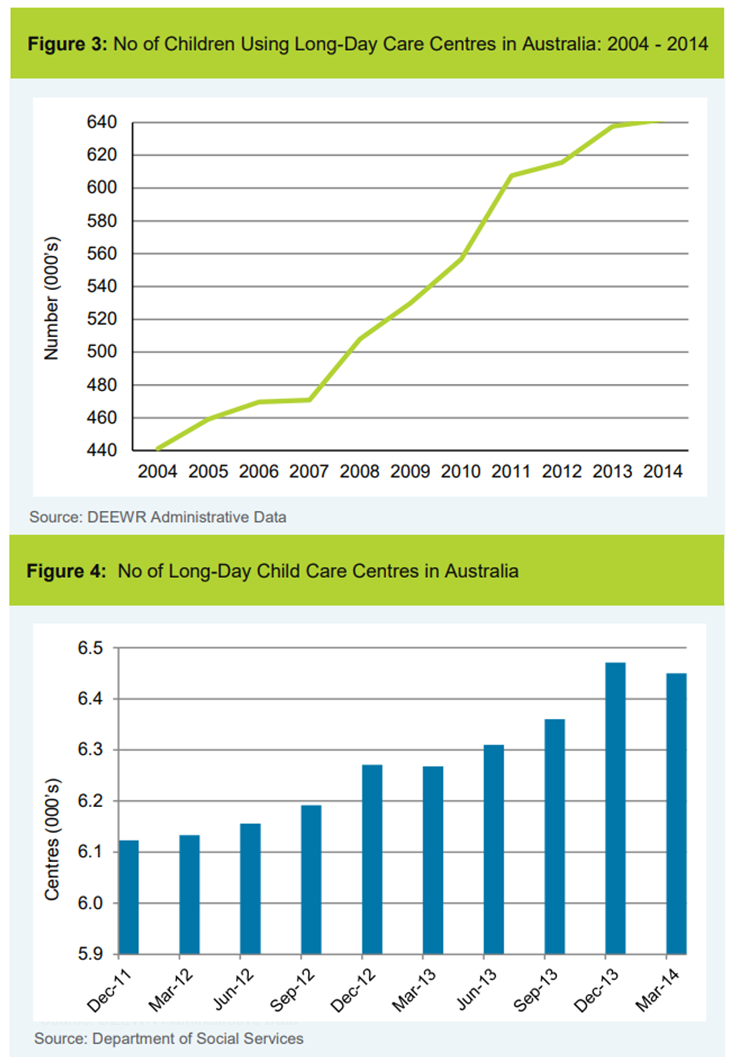

Despite an aging population, given reasonable levels of fertility rates, rising immigration levels and longer life expectancy, Australia’s overall population should continue to increase. The number of children aged 0-5 years has increased from around 1.25 million in the mid 70’s to more than 1.53 million in 2014 – an 18% increase over 30 years (Figure 2). In the next 10 years, the ABS forecast that the number of 0 – 5 year olds is projected to increase to just under 2.1 million children2. An additional 0.5 million 0 - 5 year olds will have a significant impact on demand for early learning places.

There is a growing body of research that shows quality education and care early in life leads to better health, education and employment outcomes later in life. As a result, more children are being enrolled in, and spending more time at, early learning centres placing increased demand on early learning services.

The Early Learning Sector

In response to these demographic and socio-economic trends together with shifts in public policy including national quality frameworks and standards and increased government funding, the early learning sector in Australia has grown from a small, fragmented ‘cottage industry’, characterised by separate mostly community-driven child care to a diverse industry comprising predominantly for-profit but also not-for-profit services.

The National Quality Framework (NQF), an agreement between all Australian governments to work together to provide better educational and developmental outcomes for children using education and care services, has implemented a series of quality standards including one devoted to the physical environment of centres.

In addition, the design and layout of early learning centres and the care environment are also improving in response to significant enhancements in the delivery of early learning education programs and practices.

Since 2004, the number of children using long day care child care has increased by 45% from 441,240 to 641,7403 (Figure 3).

As at March 2014, there were approximately 6,450 long day care centres in Australia, an increase of 1,893 centres or 42 per cent since 20043 (Figure 4).

Despite the large increase in the number of centres, there continues to be unmet demand, as evidenced by lengthy waiting lists, in many areas across Australia. According to the Department of Education finding child care can be particularly difficult in some areas, such as inner-city suburbs and mining towns, where the cost of entry and operation for service providers outweighs the communities’ and parents’ capacity to pay, even after subsidies and other assistance from government4. In inner-cities, land costs and availability are significant constraints on the supply of centres. This is particularly the case in areas where land has a higher value as medium or high density housing or office space rather than for educational uses such as child care.

In regional areas where rents are typically lower and land more readily available, the main constraint on supply is the availability of educators.4

Government support of the sector

Access to affordable early learning is a critical issue for most Australian families. Without financial assistance, many families would find the cost of child care to be prohibitive.

Australian, State and Territory government expenditure on early learning has increased substantially in recent years – increasing 80% or $3 billion in real terms between 2007-08 and 2012-135. In 2014-15, government expenditure is expected to be more than $8 billion.

The strongest growth in expenditure is for the Child Care Rebate (CCR) and Child Care Benefit (CCB), which are aimed at supporting parents with the cost of child care and also encouraging higher workforce participation.

The CCR covers families for 50% of their out of pocket approved child care expenses after the CCB has been received, up to a maximum limited per child of $7,500 per year. The CCR is available regardless of family income and is focused on supporting workforce participation, with the rate set relative to out of pocket costs. The CCB is targeted towards lower income earners, through means testing, and has a range of rates depending on family income, the number of children in care and the type of care used. Both subsidies are ‘demand-driven’, which means they respond to demand from families for approved child care.

In the 2014-2015 Budget, $3.14 billion is forecast to be spent on the CCB, increasing to $3.72 billion by 2017-20186. The Government has also forecast to spend $3.16 billion on the CCR in 2014-2015, and increasing to $4.32 billion by 2017-2018.

The Government has also forecast in the 2014-2015 Budget that the number of children using approved child care places (including long day care, family day care and other forms of care) is set to increase from 1.43 million in 2013-2014 to more than 1.72 million by 2017-2018, which as noted earlier will have a significant impact on the demand for child care places.

Why Folkestone continues to invest in early learning centres

Early learning centres are an attractive real estate investment given:

- the high yield’s – Folkestone’s centres typically yield between 7.5%and 8.5%;

- the lease structure - a combination of a long duration initial lease term of circa 15 years (the current Folkestone portfolio average is 8.4 years), inflation protection given rental increases are typically linked to CPI changes and a triple-net structure which means that all capital expenditure and refurbishments related to the centre are paid by the tenant;

- the quality of early learning centres is improving – newer centres are high quality purpose built centres rather than the ‘converted residential premises’;

- tenants are inherently linked to their premises due to the specialised nature of the centres;

- the on-going demand for early learning and child care places;

- government support of the sector; and

- significant long term alternate use prospects, particularly for medium density housing.

1 Daley, John (Grattan Institute), Game Changers: Economic Reform Priorities for Australia, June 2012

2 ABS - 3222.0 - Population Projections, Australia, 2012 (Base) to 2101

3 Department of Social Services – Child Care & Early Learning in Summary – March Quarter 2014

4 Department of Education - Submission to the Productivity Commission’s Inquiry into Child Care and Early Childhood Learning – February 2014

5 Productivity Commission Inequity Report – Childcare and Early Childhood Learning – Vol 1 – October 2014

6 Commonwealth of Australia – Portfolio Budget Statements: 2014-2015

Related News

Charter Hall acquires $445 million Sonic Healthcare life science facility on a 20-year triple-net sale and leaseback

Read more.tmb-news.jpg?Culture=en&sfvrsn=96db9902_1 "Office")

APPF Commercial and Charter Hall reach agreement on Sydney CBD assets

Read more

Charter Hall and WSI secure O’Brien as first anchor tenant at Western Sydney International Airport Business Precinct

Read moreTalk to us

Thanks for your interest in Charter Hall. Fill in your details below and we’ll get back to you as soon as possible.

I am interested in

Enquiry

*Indicates that this field is required.

All personal information submitted will be treated in accordance with our privacy policy.

By registering and/or submitting personal data to Charter Hall, you agree that, where it is permitted by law and in accordance with our Privacy Statement or where you have agreed to receive communications from us, Charter Hall may use this information to notify you of our products and services and seek your feedback on our products and services. Please note you can manually opt out of any communications.

-

© Charter Hall Group, 2026.

- Terms of Use

- Privacy Policy

- Complaints Guide