Beyond Core Real Estate Investing – What are the Opportunities?

LINKEDIN

LINKEDIN

FACEBOOK

FACEBOOK

TWITTER

TWITTER

EMAIL

EMAIL

31 mins

31 mins

Download

Download

Share

Share

By proceeding you confirm that you are a resident of Australia or New Zealand accessing this website from within Australia or New Zealand and you represent, warrant and agree that:

- you are not in the United States or a “U.S. person”, as defined in Regulation S under the U.S. Securities Act of 1933, as amended (“U.S. Person”), nor are you acting for the account or benefit of a U.S. Person;

- you will not make a copy of the documents on this website available to, or distribute a copy of such documents to, or for the account or benefit of, any U.S. Person or any person in any other place in which, or to any other person to whom, it would be unlawful to do so; and

- the state, territory or province and postcode provided by you below for your primary residence in Australia or New Zealand are true and accurate.

Unfortunately, legal restrictions prevent us from allowing you access to this website. If you have any questions, please contact us by e-mail by clicking on the link below.

Over the past 20 years, the real estate universe has grown considerably in both its scope and complexity. Real estate has gone global, has transcended both public and private debt and equity markets and expanded to include alternative ‘niche’ real estate types and investment strategies based on different risk/return outcomes.

Despite this, most investors became risk averse post the GFC. As a result, unprecedented levels of capital have flowed into prime office, retail and industrial assets in the major markets in the chase for secure income, driving significant competition for prime assets and a firming of yields.

The more astute investors are now coming to the conclusion that pricing for stabilised unlevered prime assets in core markets may be getting ahead of the underlying real estate fundamentals, and the risk-adjusted returns may not be as compelling at this point in the cycle. In other words, they recognise that opportunities for prime assets in core markets have become harder to find and investors are increasingly being forced to pay up for the perceived safety of these assets; in some cases, they may be taking on more risk as these prime assets are being “priced for perfection”.

Therefore, some investors are starting to look at investment strategies beyond investing in prime assets in core locations to secure attractive risk-adjusted returns.

Investors are primarily doing this in one of three ways:

- investing in non-core locations;

- broadening the definition of core income producing real estate to embrace more alternate sectors such as real estate related social infrastructure; and,

- moving up the risk curve and investing in value-added or opportunistic strategies that offer potentially higher risk-adjusted returns.

Investment strategies in the real estate sector

The role of non-residential real estate in a multi-asset portfolio has traditionally been to provide investors with stable,

predictable income, inflation hedging and diversification to equities and fixed income.

However, over the past 20 years, the real estate asset class has grown considerably in both scope and complexity. Investors now have a broader menu of investment opportunities across public and private, debt and equity markets, and investment strategies based on different risk/return profiles.

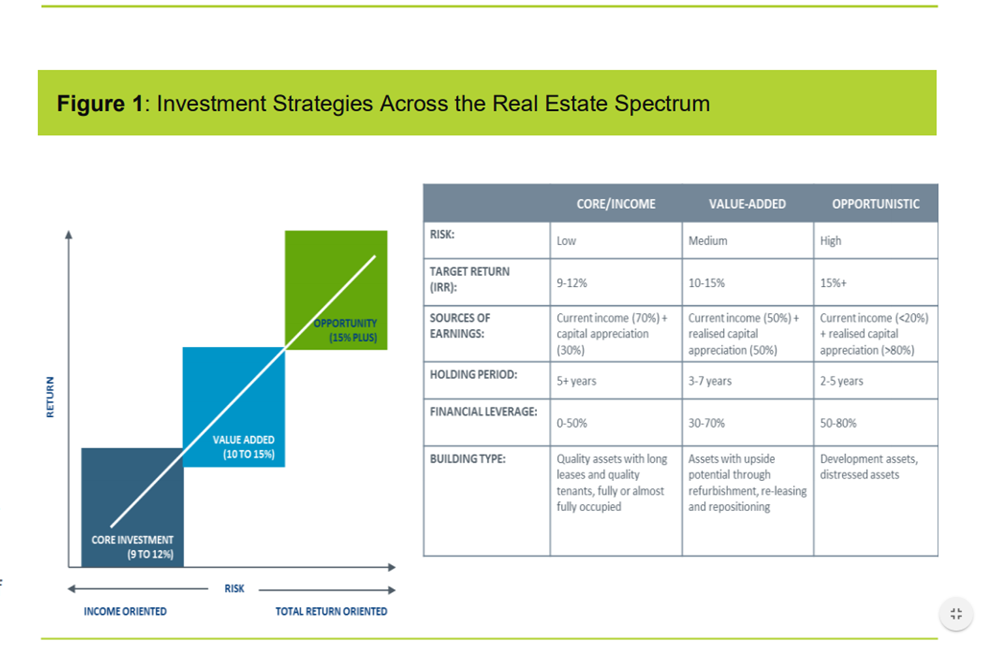

A comparison of core, value-added and opportunistic real estate investment strategies is presented in Figure 1.

The characteristics of each investment strategy differ according to risk, target returns, source of earnings, holding periods, financial leverage and asset type.

Core real estate investing is buying assets that are well leased with low levels of leverage. Such investments typically target 9-12% total returns with the objective of providing investors with stable, predictable operating income plus modest capital appreciation. Core tends to be a beta play, with a lot less opportunity to add alpha than in non-core strategies.

Value-added investing engages in active strategies to create value in the underlying investments through refurbishment, re-development, and leasing-up of vacant space. These investments target returns between 10-15% and typically use modest to high levels of leverage. The goal is to turn less than prime (secondary) assets into core real estate, which can be resold at lower yields and therefore higher capital values, and will appeal to a broader range of investors investing in just core real estate assets.

Opportunistic investing targets higher risk strategies such as development, highly leveraged financing or transactions involving highly complicated financial structures or corporate rather than asset transactions ie acquiring real estate operating businesses. Such strategies usually use higher levels of leverage and typically target returns of 15% p.a. plus, and in many cases 20% p.a. plus.

Both value-added and opportunistic investment strategies adopt shorter-term hold periods – typically less than 5 years, and in many cases less than 3 years. Holding assets too long can result in missed opportunities; the key is to exit the asset as the investment strategy is executed and value maximised.

Value-added and opportunistic investing is not simply the use of high levels of leverage in real estate strategies, it is about careful analysis of market trends and the real estate cycle to take advantage of dislocations and mispricing in the market and actively managing the asset through refurbishment, re-leasing and/or development to produce superior returns relative to the market. In other words, there is more opportunity to generate alpha from value-added and opportunistic investment strategies than core strategies. These strategies are more appropriate for investors with a higher risk tolerance.

Investing in non-core locations

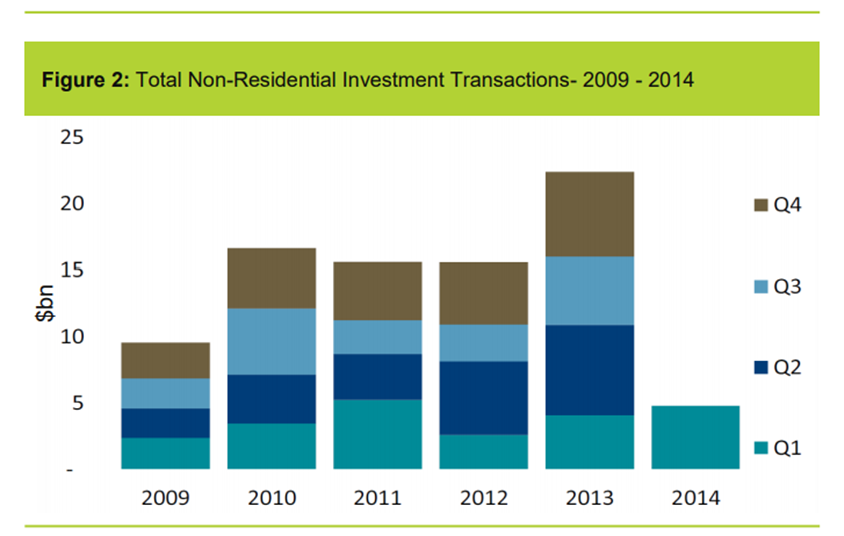

The flight to quality by investors post the GFC, has seen strong levels of capital chasing prime assets in major markets. Transactions were very strong in 2013 and this has continued into 2014 (Figure 2). According to DTZ, more than $23bn of Australian non-residential real estate transacted in 2013 and in Q1 2014, $4.8bn was transacted, up 10% on Q1 2013 volumes1. The majority of this capital flowed into prime office, retail and industrial assets.

ns since the GFC. Concerns about the depth of market, quality of tenant covenants, and the impact that shifts in supply and demand can have in smaller non-core markets has seen investors focus on the deeper, larger core markets such as the capital city CBD office markets or Sydney and Melbourne warehouse/distribution markets.

One of the benefits of looking outside the core locations is that, at this point in the cycle, there is less of a herd mentality when it comes to capital flows. And sometimes “bigger and shiny isn’t necessarily better”.

During the pre GFC boom, the risk premium for assets in secondary markets relative to core markets eroded as capital flowed across all markets. Simply put, investors were not rewarded for taking on the risk of moving out of the prime markets and or investing in secondary assets.

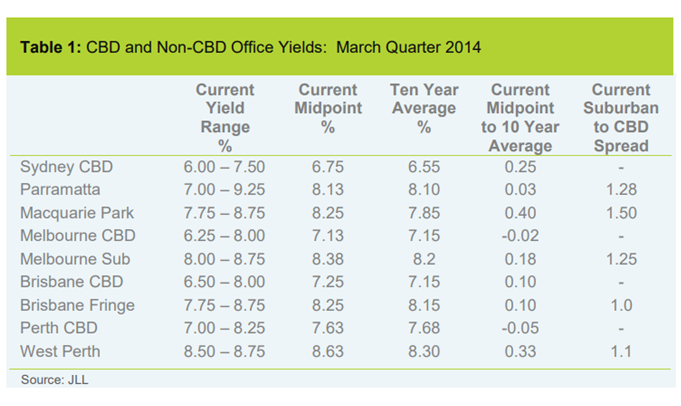

The current wide spread between the core and non-core locations as evidenced by the spread between CBD and suburban office markets suggests that suburban markets are now offering attractive pricing relative to the CBD.

Therefore, investors may now be rewarded for looking outside the major core markets. The recent launch by GPT of a suburban office fund and single asset funds by Centuria, Cromwell and Folkestone is evidence of this trend.

Table 1 shows the current yield spread between CBD and major suburban office markets. According to JLL, Sydney CBD prime office yields range from 6.0% to 7.5% (midpoint 6.75%) whereas in Macquarie Park, Sydney’s largest suburban office market, the yield range is 7.75% to 8.75% (midpoint 8.25%)2. The effective yield spread based on the midpoint yield of both markets is 150 basis points.

In Melbourne, the spread between CBD and suburban markets is 125 basis points while in Perth and Brisbane, the spread is 100 and 110 basis points respectively. The latter two markets have lower spreads as the suburban markets in both cities were targeted earlier in the cycle by investors chasing assets in these resource led markets.

A combination of factors including relative low vacancy, a moderate development outlook capping new supply and yield spreads provides an investment case for assets in non-core locations such as the suburban office markets.

But like any investment in real estate, while the top down macro view may make sense, real estate is a heterogeneous asset, therefore investors need to correctly ‘underwrite’ the investment in each individual asset in these markets.

Extending core into alternatie real estate sectors

In recent years, investors have started to embrace alternate specialised real estate sectors such as childcare, seniors housing (manufactured housing, retirement villages and aged care), student accommodation, government premises (police stations, courthouses, ambulance stations etc) and medical/health facilities. These alternate sectors are often referred to as ‘real estate social infrastructure’. As the buying opportunities for office, retail and industrial become scarcer, the underlying demand drivers and the attractive yields generated by these sectors should become even more appealing to investors over the longer-term.

The growth in real estate social infrastructure opportunities is primarily being driven by:

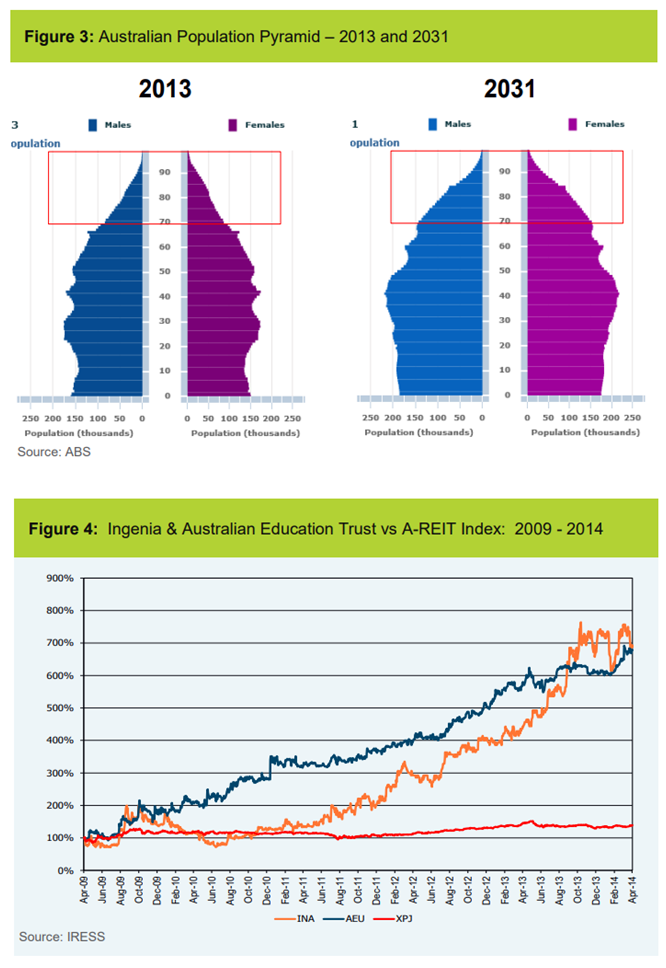

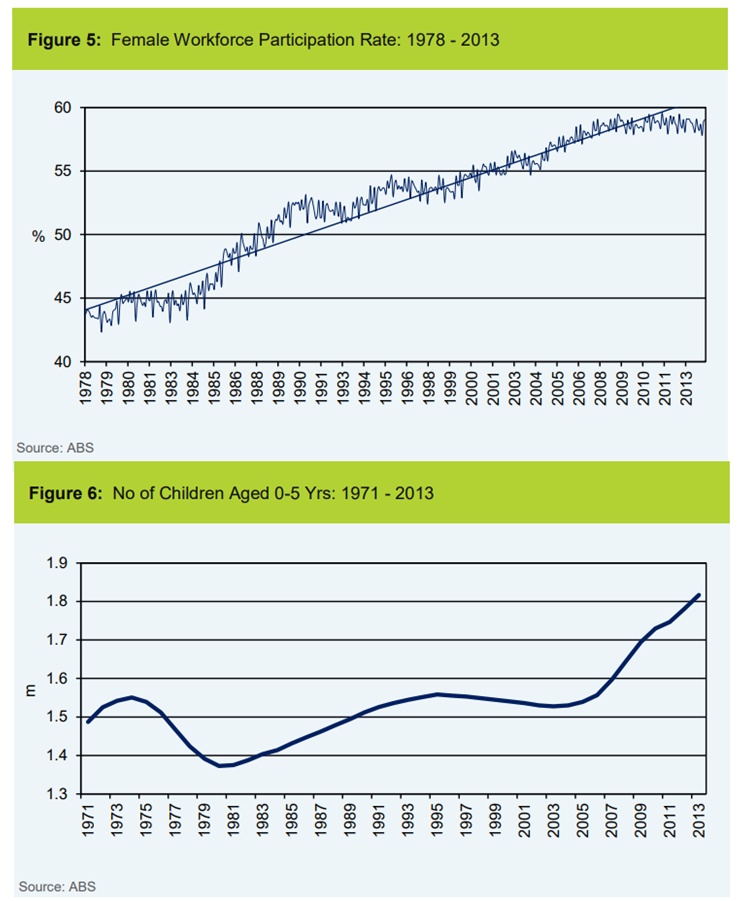

- demographic and social changes -our ageing population is increasing the demand for aged care and health services (Figure 3) while higher participation of females in the workforce (Figure 5) and the growing number of 0-5 year olds is increasing the demand for childcare (Figure 6);

- the demand for better quality facilities– the tenants/operators and their customers are requiring higher quality services and facilities.

For example, the childcare sector is moving from ‘child minding’ to early learning which is changing the design and layout of centres, the health care sector is being driven by advances in medical technology and procedures and the aged care sector, supported by government regulation on quality standards and bed places to population ratios, is increasing the demand for higher quality aged care homes; government financing/budget constraints which impact on the public sector’s ability to fund the level of infrastructure required to meet the needs of the community; relative high population growth rates and greater urbanisation of our major cities which increases the need for investment on social infrastructure assets that support communities; and the growing realisation that operators should focus on their core business of managing and delivering services to the community rather than the provision, ownership and management of the underlying real estate assets.

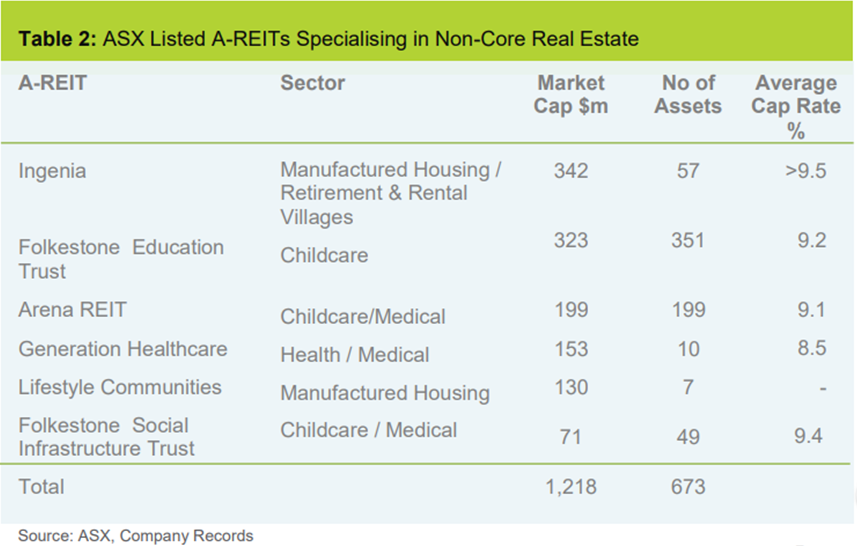

In recent years, the Australian listed real estate market (A-REITs) has embraced these alternate social real estate focused sectors more so than in the unlisted market. There are now sector specialist A-REITs in childcare, manufactured housing, retirement, aged care and health/medical (Table 2). However, theses A-REITs make up less than 0.3%of the entire listed A-REIT sector. In the US, there are 14 healthcare REITs and 3 manufactured housing REITs which represent around 11.0% of the total REIT market capitalisation3. In addition, there are three large US REITs dedicated to student housing in the US with a market capitalisation of approximately $2.7 billion.

The performance of the social real estate focused A-REITs has generally been very strong. Two of the best performing A-REITs in this space is Ingenia, the manufactured housing and retirement village group and the Australian Education Trust (Figure 4). Ingenia has generated an annualised total return of 69 per cent over the five years to April 2014 while the Australian Education Trust generated a total return of 65 per cent over the same period. By comparison the S&P/ASX300 A-REIT accumulation Index returned 16 per cent and the S&P/ASX 300 Equities Accumulation Index returned 13 per cent.

The unlisted market is also embracing the real estate social infrastructure sector but as noted earlier it is still behind the listed market. The only notable unlisted social infrastructure funds are the Australian Unity Healthcare Fund which owns more than $540 million of hospitals, medical clinics, nursing homes, day surgeries, consulting rooms, rehabilitation units, radiology and pathology centres, the Folkestone managed CIB Fund which owns a portfolio of police stations and courthouses leased back to the Victorian government and the Transfield managed Campus Living Villages Fund which owns a portfolio of student accommodation facilities.

The benefits of investing in social infrastructure typically include longer leases than traditional real estate assets (often 10 years or more), net or triple net leases (whereby the operator/tenant pays outgoings and is responsible for repairs and maintenance), secure, often government backed, cash flows and low correlation and relative lower volatility to other real estate and non-real estate assets.

The benefits of social infrastructure assets need to be considered in light of the risks. As with any investment, there are some drawbacks to pursuing these types of assets. That’s not necessarily a reason to avoid them but investors need to understand and appropriately price and manage these risks.

The key risk investors identify is the specialised nature and often the critical importance of the operator leasing the asset. Owning a private hospital is a very specialised asset and having a well-capitalised and competent hospital operator such as Ramsay Health Care or Healthscope is critical.

In addition, successful investing in this sector requires a sound relationship between the operator (sometimes a government agency) and the real estate owner. While the increased operating leverage and other industry risks clearly warrant a risk premium, the sectors risk-reward profile has improved greatly as many of these social infrastructure sectors have grown and matured. For many of them, they are no longer at cottage industry.

Consolidation of operators in the childcare and health sector is well underway – with many of the operators publicly listed companies such as G8 and Affinity in the childcare space and Ramsay Health Care and Primary Health Care in the health care space and Japarra (listed on April 18) in the aged care space.

Also, with sectors such as child care and seniors living, investors are relying, to some extent, on high levels of government regulation and intervention which are susceptible to change. However, this can also be a positive, especially if the government is partially or fully underwriting the cashflows of the sector.

Recent activity indicates that investors are increasingly willing to invest in real estate social infrastructure so long as the investment can deliver an acceptable risk-adjusted return.

Whilst we are a long way from there yet, it should be acknowledged that there may simply not be enough acquisition opportunities to satisfy the demand for assets if these alternate real estate social infrastructure sectors go mainstream.

The market is limited in terms of the number of potential assets in some sectors, and given the smaller number and often their specialised nature, these assets are often less liquid than an office building or retail centre, making it difficult for the larger institutional investors to get set. Also, like any sector, if the hot money starts chasing these assets, prices may rise too quickly, and yields fall, reducing their attractiveness.

Childcare centres

Demographic and socio-economic changes will continue to drive the demand for childcare. Childcare is now seen as both a mechanism to support labour force participation, particularly driven by the increase in female participation in the workforce (Figure 5) and an important form of early learning and education. In addition, increases in fertility rates and net immigration should continue to increase the number of 0-5 year olds that require access to childcare (Figure 6).

As at September 2012, there were approximately 6,192 long day care centres in Australia, an increase of 1,635 centres or 35.9 per cent since 20044. At the same time, the number of children using long day care centres has increased by 39.5 per cent to 615,630 children4. Almost half (49.2 per cent) of 3 to 5 year olds used childcare in 2012, up from 43.0 per cent in 2006. In the 0-2 years age cohort, 31.4 per cent use childcare compared to 26.9 per cent in 2006.

Access to affordable early learning and long waiting lists are critical issues for most Australian families. Despite the increase in the number of centres in recent years and significant government funding to the sector there continues to be unmet demand, as evidenced by lengthy waiting lists, in many areas across Australia.

Early learning centres are an attractive real estate investment given:

- the high yield’s – childcare centres typically yield between 8.0 per cent and 9.5 per cent;

- the lease structure - a combination of a long duration initial lease term of between 10 and 15 years, inflation protection given rental increases are typically linked to CPI changes and a triple-net structure which means that all outgoings, repairs and maintenance and refurbishments related to the centre are paid by the tenant;

- government support of the sector; and

- the on-going demand for early learning and childcare places.

Student Accomodation

The number of students graduating from university is increasing as is the number of foreign students enrolling in Australian universities. The Federal Government’s International Education Advisory Council released a report in February 2013 that forecast a 30 per cent increase in international students to 117,000 by 20205.

Another key driver of demand is a lack of university capital and expertise to develop or manage new on-campus facilities.

Attractive student housing opportunities are likely to be found in both major capital cities and regional towns which have large universities such as Armidale, Townsville and Wollongong.

Until recently, this was a highly fragmented market with few established players. Now local players such as Unilodge, Iglu and Campus Living Villages, together with international operators such as Urbanest are making their presence felt in the Australian market.

In the UK and US, student accommodation has been well supported by both private and institutional investors with investors expected to increase their portfolio allocation to this asset class driven by the less cyclical performance of student accommodation.6 Australia still lags behind these markets.

Health and Medical Facilities

With increasing demand for healthcare services, there comes a greater need for healthcare infrastructure. A rapidly growing and ageing population together with changes in the delivery of healthcare services is driving the demand for health and medical related real estate. Two changes that are gaining momentum is the creation of new multi-tenant one stop shop health facilities, similar to the way regional shopping centres bring retailers under one roof and both Federal and State governments increasingly looking to the private sector to provide healthcare services to reduce the burden on the public healthcare system.

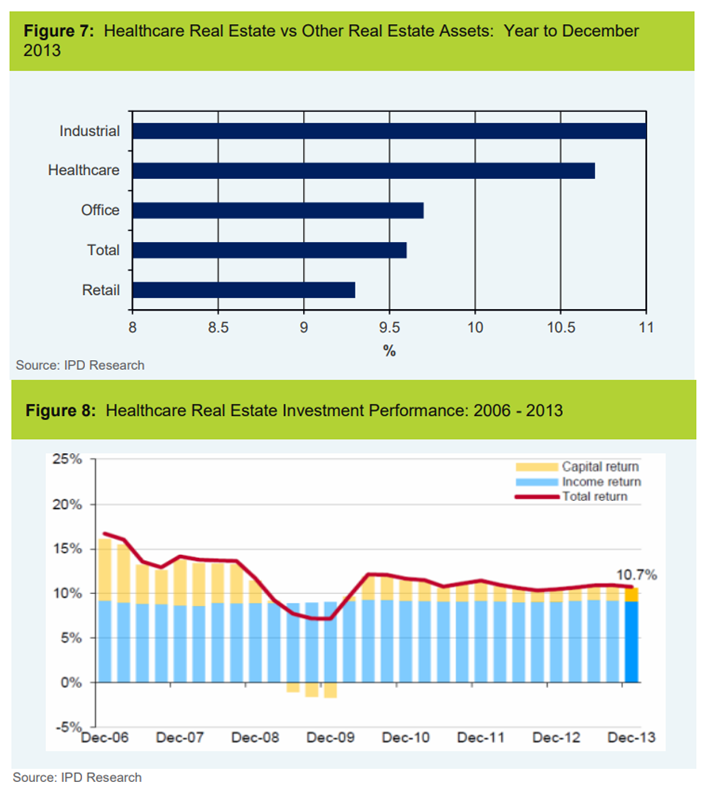

Healthcare is the only alternate real estate sector that has an established investment performance benchmark – the PCA/IPD Australian Property Index – which tracks the performance of more than $1.4 billion of assets across medical hospitals, rehabilitation hospitals, medical centres and aged care facilities (nursing homes).

According to the Index, healthcare generated a total return of 10.7 per cent in the year to December 2013, outperforming office (9.7 per cent), retail (9.3 per cent) and marginally under-performing industrial (11.0 per cent) (Figure 7).

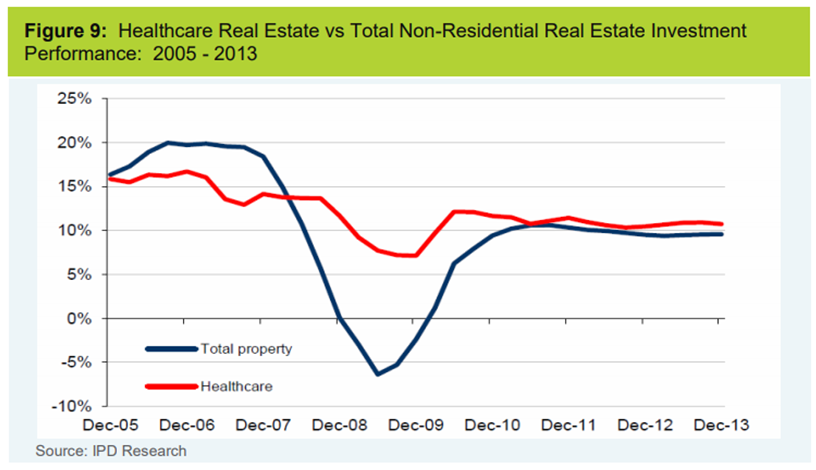

As a result of the strong underlying income, typically longer term leases and the fact that demand in this sector is more resilient in the face of economic and real estate market downturns, the volatility of returns compared to the overall non-residential real estate market is significantly lower (Figure 9).

Seniors Living

Over the longer term demand for seniors living should accelerate dramatically as the baby boomer generation reaches retirement age and life expectancy continue to increase. The seniors housing industry includes a wide range of facilities that provide varying levels of lifestyle support and health care services to residents. Facilities range from independent living (manufactured houses and retirement villages) that provide minimal or no special services for active retirees to specialised care facilities such as nursing homes that offer 24 hour assistance and medical care.

Projections by the ABS indicate the number of people aged over 65 is forecast to increase from 3.2 million at 30 June 2012 to between 5.7 million and 5.8 million in 2031, and to between 9.0 million and 11.1 million in 2061.7

One of the fastest growing segments of seniors living is the manufactured housing estate MHE’s. A MHE is a parcel of land where the land is owned by an entity and the land is divided into “lots” where the land owner rents out these lots to owners of manufactured homes. Tenants who own manufactured homes will bring their home into a MHE or buy an existing home in the estate and sign a lease agreement to lease the land for a period of time – typically 3 years.

The owner of the manufactured housing estate collects rent every month from tenants, in exchange for the right to have their home located on their designated lot, connect to the estate’s infrastructure (electrical, water, gas and sewer line connections) and use the estate’s facilities (BBQ’s, pool, recreation hall etc).

A manufactured home is a factory built home that is typically manufactured off-site and then moved to a MHE. A manufactured home can be permanently attached to a foundation or it can be placed on blocks and tied down if the module home may be moved again in the future. Increasingly, homes are being made more permanent because they have gotten larger and are much more complicated to move.

Upon departure from the estate, if the home remains, the resident is responsible for selling their home to a new resident who enters into a new land lease with the operator.

MHE’s are a widely accepted form of housing in the US, Europe and Canada where the industry has already been corporatised. However, it is only a relatively recent phenomenon in Australia, housing around 2% of the population8 although the sector is growing as listed groups like Ingenia and Lifestyle Communities, and unlisted funds managed by Alceon.

Retirement villages are residential communities for seniors. The key difference between these and MHE’s is the resident acquires a lifetime leasehold interest from the operator in dwelling typically a unit or villa. At the time of departure, the unit or villa is resold and the departing resident will receive back their initial investment less a deferred management fee which is typically between 25 per cent and 35 per cent of the entry price depending on how long the resident resided in the village. In addition, any capital gains are split between the resident and the operator depending on the contractual terms of the lease.

According to the Retirement Living Council, in 2008, there were 1,756 retirement villages accommodating up to 150,000 residents. In 2013, this had grown to approximately 2,160 villages offering 112,296 independent living units (ILUs) and housing more than 177,000 older Australians. The Retirement Living Council forecasts further villages will be needed to be developed over the coming decades to meet the expected demand.9

Aged care facilities typically provide either or both high and low care. High level care homes (previously known as nursing homes) offer care for people with a greater frailty and who often need continuous nursing care. Low care facilities (formerly known as hostels) generally provide accommodation and personal care which includes help with dressing and showering, and occasional nursing care.

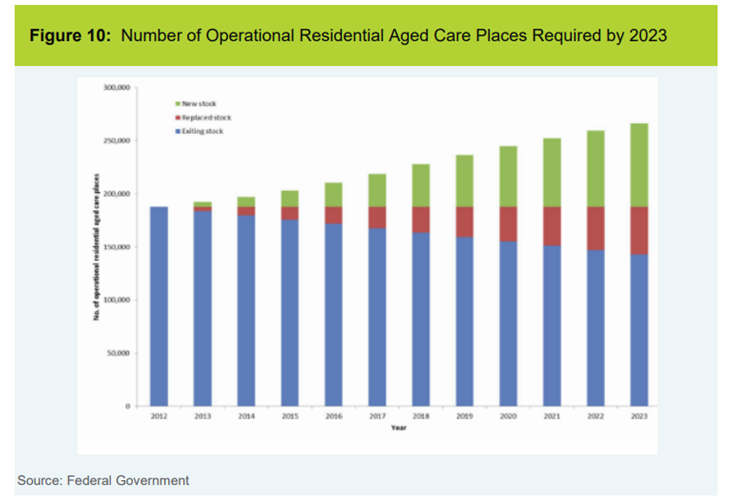

According to the Federal Government’s Aged Care Financing Authority, there are 2,716 aged care homes providing 182,663 places (beds), operated by more than 1,054 operators.10 The Government predicts that the residential aged care sector will need to build approximately 74,000 additional places over the next decade in order to achieve the Government’s desired ratio of 80 bed places per 1,000 people aged 70 and over (Figure 10). The provision of extra beds and rebuilding of about 25 per cent of the current stock is estimated to cost around $25 billion in 2011-2012 prices. As the Aged Care Financing Authority Point out “these estimates represent both a challenge and a significant opportunity. Providers need to operate at a level that encourages investment, Federal Government policies need to be supportive of investment in the sector and investors need to recognise the opportunities that the growth and demand for services will bring.”

Value-added opportunistic investing

Those investors with higher risk tolerances are moving up the risk curve to invest in value-added or opportunistic strategies.

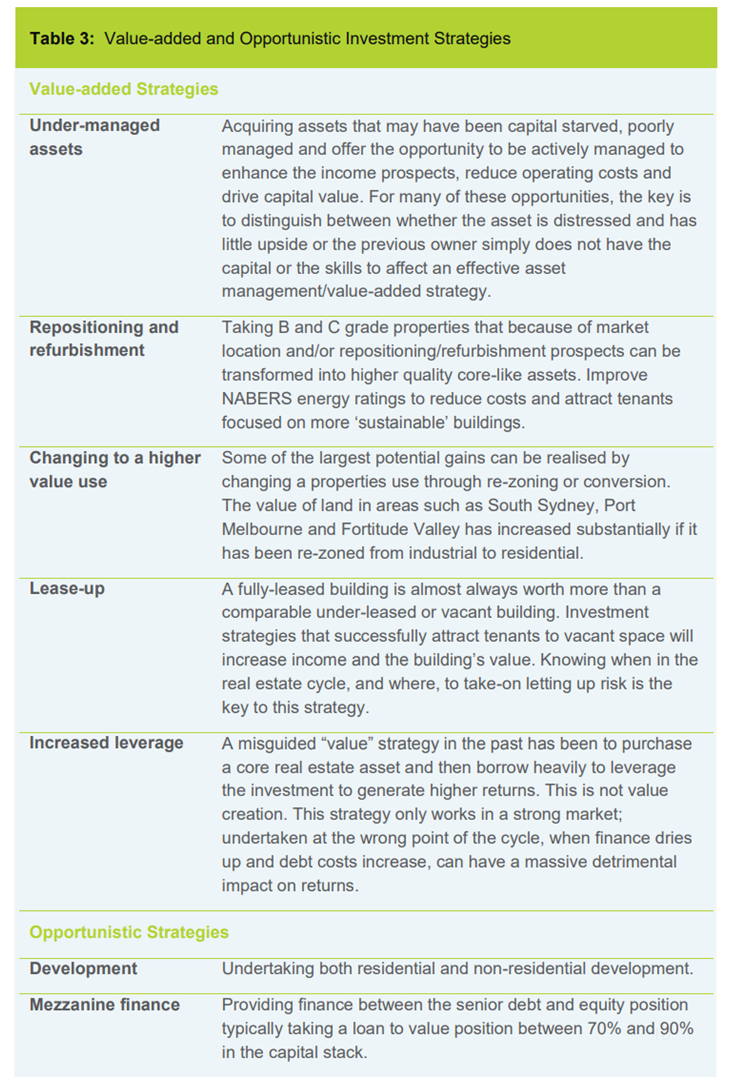

Typical value-add strategies include acquiring under managed assets, re-positioning and refurbishing an asset, changing to a higher value use, leasing up vacancy space and increasing leverage.

Opportunistic strategies include development and real estate mezzanine financing. The real estate market is relatively inefficient, assets are heterogeneous, and many investors are prepared to invest in value-added and opportunistic strategies on the basis they view the potential alpha generation warrants the additional risk being taken on with these strategies.

Table 3 provides a summary of the various value-added and opportunistic strategies.

Two strategies in the value-add and opportunistic space that will increasingly get the attention of investors in the coming year are repositioning and refurbishing assets and development especially to create core assets.

Repositioning and refurbishing non-core (secondary) assets

The growing obsolescence of investment grade stock in office and industrial markets provides a unique opportunity. According to JLL, 46% of the Sydney CBD is more than 30 years old and a high proportion of buildings are reaching the end of their effective life.11

Changing tenant requirements are driving new demands in the quality of space including large floorplates to allow more efficient workspace design and flow and more sustainable ‘green’ buildings.

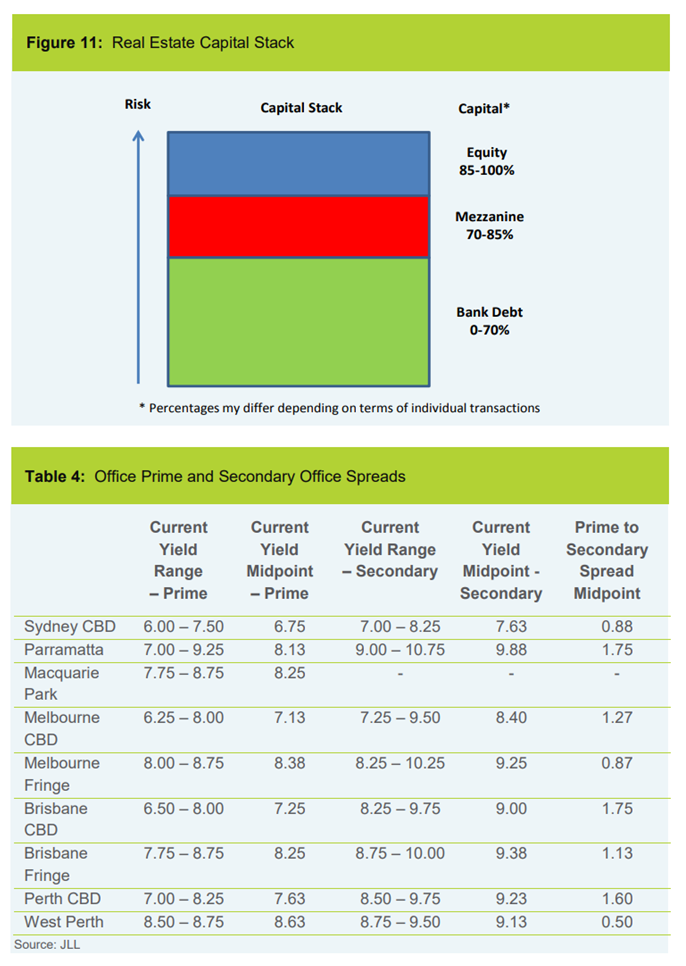

The popularity of prime assets has driven prime yields lower than secondary yields leading to a yield gap between the two (Table 4). A number of institutions and syndicators are establishing funds targeting suburban office buildings. It’s a similar story for retail and industrial assets.

The spread between prime and secondary assets is likely to persist although will narrow as investors move up the risk curve and look more closely at secondary assets.

This spread and the weight of money looking for prime assets presents a strong case for re-leasing, re-positioning and refurbishing strategies. By rejuvenating an asset, owners are able to extend the asset’s life, optimise the asset’s investment performance and keep it in the portfolio as a core asset or sell to an investor chasing quality assets.

Development - Fund throughs

Another consequence of such a competitive market is that investors are increasingly considering development as a way of adding high quality assets to their portfolios.

This can be achieved by entering into an agreement to acquire a completed project but signing either prior to construction commencing or during construction on a “fund through” basis. The developer and the investor agree terms based on the investor making a down payment (usually the cost of the land) and then making progressive payments during the construction period and a lump sum at the end based on the achievement of realised net income from the asset adjusted for any payments along the way. During the construction period, the investor will receive a coupon payment from the developer commensurate with the yield expected from the completed development on the investor’s funds employed along the way.

From the investor’s perspective, they are acquiring an asset with low transaction costs - stamp duty is payable on the land and any construction payments made prior to entering into the contract rather than on the completed value. The investor also receives ownership of a newly constructed, high quality asset, without incurring the normal risks associated with undertaking a development through mechanisms such as a fixed construction price and income guarantees supporting any vacancy on completion.

From the developer’s perspective, the development risk continues to reside with them. However, they have pre-sold the development (taking away exit risk). The developer also gets to utilise the investor’s capital during the construction phase rather than their own capital thereby reducing their equity investment and increasing their return on equity from development.

Mezzanine Financing

Opportunities are growing for investment into new real estate debt based funds, which can provide investors into the funds an alternative way of investing in real estate with attractive risk adjusted returns. One particular avenue is mezzanine finance. Mezzanine finance has become an important source of capital for real estate acquisitions, development, and refinancings, as traditional first mortgage providers (the banks) have become more reluctant to finance projects at loan-to-value (LTV) ratios in excess of 65% for income producing assets and 70% for developments. The increased conservatism of lenders, partly in response to regulatory requirements and partly in response to the lessons learnt from the GFC has created a gap between what lenders will provide and the amount of equity borrowers are prepared to put into a deal.

The result has been increased segmentation of the capital structure for specific real estate transactions. In structuring the equity and debt in a real estate transaction, the prioritisation of capital achieved between the parties is often called the capital stack. Although theoretically there can be many layers, the capital stack can generally be divided into three distinctive groupings: senior debt typically provided by a bank, sub-ordinated debt and equity (Figure 11). Sub-ordinated debt structures have many definitions in the market, such as mezzanine, subordinated loans, and B notes.

Generally, mezzanine financing takes the form of a second mortgage loan that provides the financing from between 70 to 85 percent of the total capital requirements – in some cases, mezzanine may go as higher as 90 per cent although since the GFC, lenders have required more equity in deals.

Mezzanine lenders require that they get paid from first available cash flow after the senior debt and before the borrower gets any real distributions. In recognition of this prioritisation, returns are structured in a way that reflects the different risks being taken by the counterparties. The challenge for finance providers is to price the mezzanine segment to provide compensation for the risk taken.

Generally, the returns for mezzanine debt run from 15 per cent and higher, depending how high up in the capital structure the mezzanine investor is contributing and the perceived risk of the underlying investment i.e. whether it be for a stabilised income producing asset or a development project. Some may view mezzanine finance as an expensive form of debt, since it attracts interest at significantly higher rates than that of senior debt. In reality, however, mezzanine financing is a substitute for equity and for developers in particular chasing development returns of 25 per cent plus, it is often viewed as cheap equity.

The underlying real estate risks are still fundamental to each tranche in the capital stack. Each investment carries a combination of structural (prioritisation) and real estate (income and capital risks). It is vitally important to concentrate on sound real estate fundamentals, together with a high attention to detail in documenting, executing and managing each individual investment.

Conclusion

As long as capital continues to flow to prime real estate assets in core sectors and locations, astute investors will increasingly search for alpha by adopting strategies that embrace alternate real estate sectors or move up the risk curve to value-added and opportunistic investments that offer compelling risk-adjusted returns. How much, and how far, investors allocate to these areas will depend on each individual investors’ investment objective, risk tolerance and liquidity requirements.

Several alternate real estate sectors such as child care, student accommodation, seniors living and medical/health offer value to investors who are prepared to expand their definition of core real estate to include these sectors. Demand is being underpinned by positive demographic trends and given these assets typically offer higher yields and longer term leases than comparable assets in the more traditional core sectors suggests that interest and capital flows in these assets is expected to keep growing.

Investors should be careful of moving up the risk curve without thinking through the strategy. Investing beyond the traditional core sectors requires a clearly articulated investment strategy and a comprehensive understanding of real estate markets to make sure the diversification benefits and the risk adjusted return potential are assessed appropriately.

Investors looking to use a manager to execute on their real estate investment strategies need to understand that careful manager selection continues to be critical to performance. To be successful, investors need to carefully choose managers who have a demonstrated ability to identify favourable market trends, can access deal flow, preferably off-market while having the depth of knowledge and skills to develop and then execute on their strategies in the particular market or sector.

Finally, investors whether investing directly or via a manager, must have the ability to constantly reassess the real estate investment environment. Disciplined investors and managers must have the patience to determine and execute market-appropriate investment strategies. Today, that means being constantly aware of the looming shadow that the weight of money effect has on real estate values and investment performance.

Related News

.tmb-news.jpg?Culture=en&sfvrsn=96db9902_1 "Office")

APPF Commercial and Charter Hall reach agreement on Sydney CBD assets

Read more

Charter Hall and WSI secure O’Brien as first anchor tenant at Western Sydney International Airport Business Precinct

Read more

Charter Hall completes $50 million estate in Adelaide, 100% pre-leased to blue-chip companies

Read moreTalk to us

Thanks for your interest in Charter Hall. Fill in your details below and we’ll get back to you as soon as possible.

I am interested in

Enquiry

*Indicates that this field is required.

All personal information submitted will be treated in accordance with our privacy policy.

By registering and/or submitting personal data to Charter Hall, you agree that, where it is permitted by law and in accordance with our Privacy Statement or where you have agreed to receive communications from us, Charter Hall may use this information to notify you of our products and services and seek your feedback on our products and services. Please note you can manually opt out of any communications.

-

© Charter Hall Group, 2026.

- Terms of Use

- Privacy Policy

- Complaints Guide